Medicare

Medicare, the federal health insurance program that currently covers 50 million Americans who are:

Medicare, the federal health insurance program that currently covers 50 million Americans who are:

- 65 years of age or older

- People under 65 with certain disabilities

- People of any age with end-stage renal disease (ESRD) (permanent kidney failure requiring dialysis or a kidney transplant)

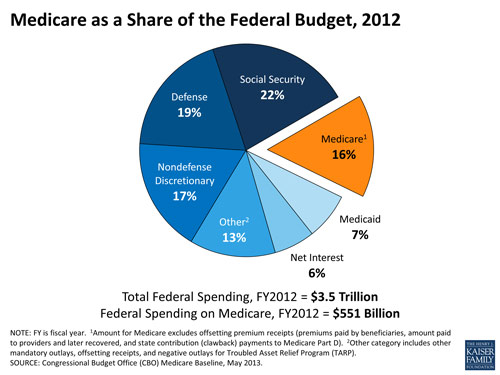

Medicare helps to pay for hospital and physician visits, prescription drugs, and other acute and post- acute services. In 2012, spending on Medicare accounted for 15% of the federal budget. Medicare also plays a major role in the health care system, accounting for 21% of total national health care spending in 2012, 28% of spending on hospital care, and 24% of spending on physician services.

The Medicare program is comprised of four parts - Part A, Part B, Part C (also known as Medicare Advantage), and Part D. Together, these four parts provide coverage for basic medical services and prescription drugs. A Medigap (Medicare Supplement Insurance) policy to help pay some of the health care cost "gaps" (like copayments, coinsurances, and deductibles) can be purchased privately.

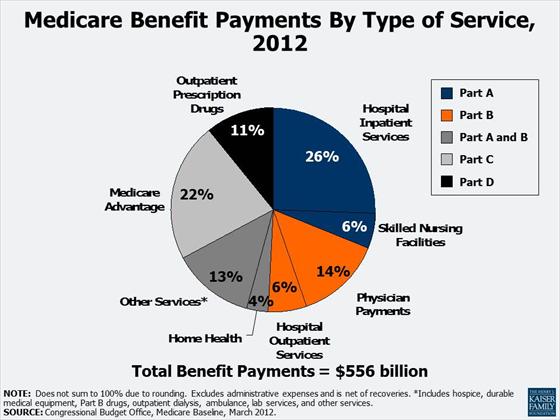

Medicare benefit payments are expected to total $556 billion in 2012; roughly two-thirds is for Part A (Hospital Insurance, or HI), and Part B (Supplementary Medical Insurance, or SMI) services. More than 20% is for Part C, Medicare Advantage private health plans covering all Part A and B benefits, and just over 10% is for the Part D drug benefit.

Medicare spending per beneficiary is highly skewed, with the top 10% of beneficiaries in traditional Medicare, accounting for 57% of total Medicare spending in 2009 - on a per capita basis, more than five times greater than the average across all beneficiaries in traditional Medicare ($55,763 vs. $9,702).

|

These are brief summaries of Medicare A, B, C, and D. |

|

This content requires JavaScript enabled.

|

|

Source: www.medicare.gov/navigation/medicare-basics/medicare-benefits/medicare-benefits-overview.aspx

Medicare Part A (Hospital Insurance)

Coverage: Part A covers inpatient hospital care, some skilled nursing facility stays, home health care, and hospice care. If you or your spouse have worked for at least 40 quarters (10 years) and paid Medicare payroll taxes, you qualify for Part A coverage, and you don't have to pay a monthly premium for it. This is referred to as "premium-free Part A."

Funding: Part A is paid for by a portion of Social Security tax. Most people pay no premium because the individual or his/her spouse paid Medicare taxes while working in the US

A Medigap (Medicare Supplement Insurance) policy to help pay some of the health care cost gaps (like copayments, coinsurances, and deductibles) can be purchased privately.

Medicare Part B (Medical Insurance)

Coverage: Part B, or the Supplementary Medical Insurance (SMI) program, helps pay for physician services, outpatient hospital care, and some home health visits not covered under Part A. It also covers laboratory and diagnostic tests, such as X-rays and blood work; durable medical equipment, such as wheelchairs and walkers; certain preventive services and screening tests, such as mammograms and prostate cancer screenings; outpatient physical, speech and occupational therapy; outpatient mental health care; and ambulance services.

Funding: People who elect Part B must pay a monthly premium. Most people who pay a Part B premium have it automatically deducted from their Social Security check. If your income is limited, you may qualify for programs that will pay the Part B premium on your behalf. The standard monthly Part B premium in 2012 is $99.90. Some people on Medicare with higher annual incomes (more than $85,000/individual; $170,000/couple) pay a higher monthly Part B premium, ranging from $139.90 to $319.70 per month in 2012, depending on their income.

Part B also has an annual deductible of $140 in 2012 - i.e., you must pay $140 out-of-pocket before Medicare begins paying. After you meet the deductible, most Part B services require a 20 percent coinsurance; this means you pay 20 percent of the cost of the service. If a doctor is a "participating provider" then the most he or she can ever charge you is 20 percent of the Medicare-approved amount for a service. This is called "accepting assignment."

Medicare Part C (Medicare Advantage)

Coverage: Part C allows beneficiaries to enroll in a private insurance plan, called a Medicare Advantage plan. Medicare Advantage plans are managed care plans, such as Health Maintenance Organizations (HMOs) or Preferred Provider Organizations (PPOs). Medicare Advantage plans must cover all Part A and B services and usually include Part D (prescription drug coverage) benefits in the same plan. These plans sometimes cover additional benefits not covered by traditional Medicare, such as routine vision and dental care. All plans have an annual limit on your out-of-pocket costs for Part A and B services, and once you reach that limit, you pay nothing for covered services for the rest of the calendar year. The out-of-pocket limit can be high but may help protect you if you need a lot of health care or need expensive treatment. Out-of-pocket costs include deductibles, copayments and coinsurance.

Although Medicare Advantage plans must cover Part A and B services, they can have different rules, costs and restrictions. Some plans have higher cost-sharing requirements than Original Medicare for some services, and most plans apply restrictions that limit your choices of doctors or hospitals.

Funding: Medicare pays a fixed amount for your care each month to the companies offering Medicare Advantage Plans. These companies must follow rules set by Medicare. However, each Medicare Advantage Plan can charge different out-of-pocket costs and have different rules for how you get services (like whether you need a referral to see a specialist or if you have to go to only doctors, facilities, or suppliers that belong to the plan for non-emergency or non-urgent care). These rules can change each year.

Medicare Part D (Prescription Drug Coverage)

Coverage: In 2006, Medicare began offering outpatient prescription drug coverage under Medicare Part D. Medicare drug coverage is optional for most people with Medicare and is offered only through Medicare private plans. If you have Original Medicare and want Part D drug coverage, you can get a stand-alone prescription drug plan (PDP). People who want a Medicare Advantage plan and drug coverage must generally get it through one plan called a Medicare Advantage prescription drug plan (MA-PD).

Funding: There is a monthly premium for Part D. Premiums vary widely among plans, as do the drugs that are covered and the amounts charged for prescriptions. The standard Part D benefit has a deductible, which in 2012 can be no more than $320, and 25 percent coinsurance on covered drugs up to an initial coverage limit. This is followed by a coverage gap, during which enrollees are responsible for a larger share of their total drug costs than during the initial coverage period, until they reach the catastrophic coverage limit. Thereafter, enrollees have low costs for their drugs.

For more complete information about Medicare, see the following publication "Talking About Medicare - Your Guide to Understanding the Program" by the Kaiser Family Foundation (updated 2012)"

![]()

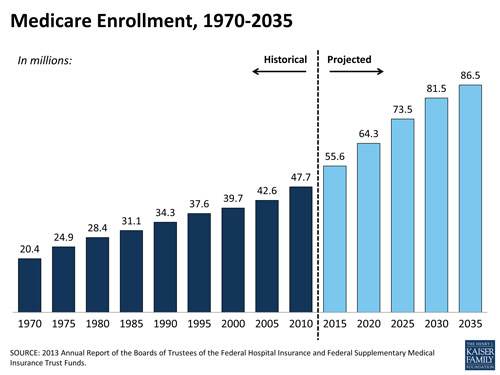

Medicare Expenditures

|

|

|

Medicare takes up a significant chunk of federal spending (remember states do not pay for Medicare). There is increasing concern because as the US population ages and life expectancy increases enrollment in Medicare will grow. See below.

Medicare is the federal health insurance program for 54 million people ages 65 and over and people with permanent disabilities. In 2013, spending on Medicare was $492 billion and accounted for 14% of the federal budget. Medicare also plays a major role in the health care system, accounting for 20% of total national health spending in 2012, 27% of spending on hospital care, and 23% of spending on physician services

Additional Resources:

- Medicare module from kaiserEDU.org

- An Overview of the Medicare Program and Medicare Beneficiaries Costs and Service Use; Statement of Juliette Cubanski, Ph.D., Associate Director, Program on Medicare Policy, The Henry J. Kaiser Family Foundation Before the Special Committee on Aging U.S. Senate, "Strengthening Medicare for Today and the Future", February 27, 2013

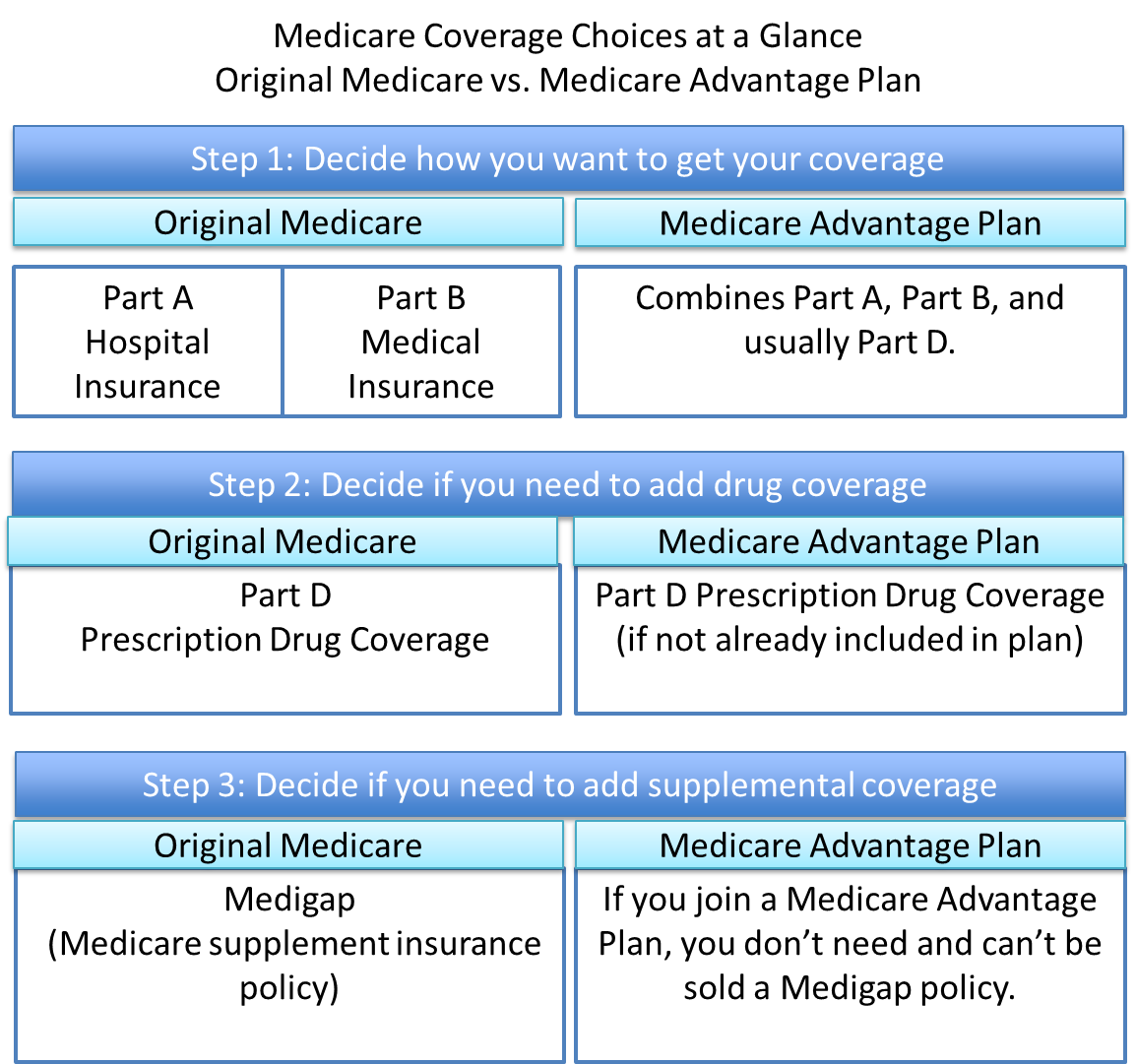

Medicare Coverage Choices at a Glance

There are two main ways you get Medicare coverage: Original Medicare or a Medicare Advantage Plan. These steps help determine which coverage to get.

Medicare Coverage Exercises

Utilize this PDF file below on Medicare Coverage Basics to analyze and calculate Medicare coverage in the situations listed below. Generate a list of costs for which the beneficiary is responsible (out-of-pocket costs). Assume both patients have Medicare A and B.

![]()

Source: developed by Mary Palaima, PT, MBA, EdD, Clinical Assoc. Professor at Sargent College of Health and Rehabilitative Sciences

|

Patient #1: A 68 y.o. female who had a stroke with multiple medical complications. She spent 65 days in the hospital, followed by 25 days in a local SNF (Skilled Nursing Facility), and then received home health services (nursing, PT, OT, SLP) for 21 days. |

Patient #2: This woman had a stroke with medical complications. She spends 14 days in the hospital followed by 40 days in a local SNF, and then receives 50 visits of PT, OT, SLP as an outpatient. Assume the charge for each therapy visit is $100.00. |

Medicare Quiz

Take this short quiz to see how much you remember!

If you would like more information about Medicare check these three sites:

- The Commonwealth Fund site for Medicare

- The US government Medicare site aimed at consumers

- Kaiser Family Foundation Medicare site